Your Child’s Tomorrow Starts Now

Get $100 towards your RESP when you start saving with us

Knowing is half the battle

We’re Here to Help You Help Them

At Embark, education savings and planning is all we do. Our sole purpose is to help students realize their full potential by simplifying your savings with tools, advice, and an RESP plan that works for your family.

Saving for the Future Has Never Been Easier

- A plan that automatically adjusts to your timeline

- Simple, expert guidance helps make investing easy

- An innovative digital platform puts education savings at your fingertips

- Ability to share your plan between your children

Simplifying RESPs

Create Your Tomorrow

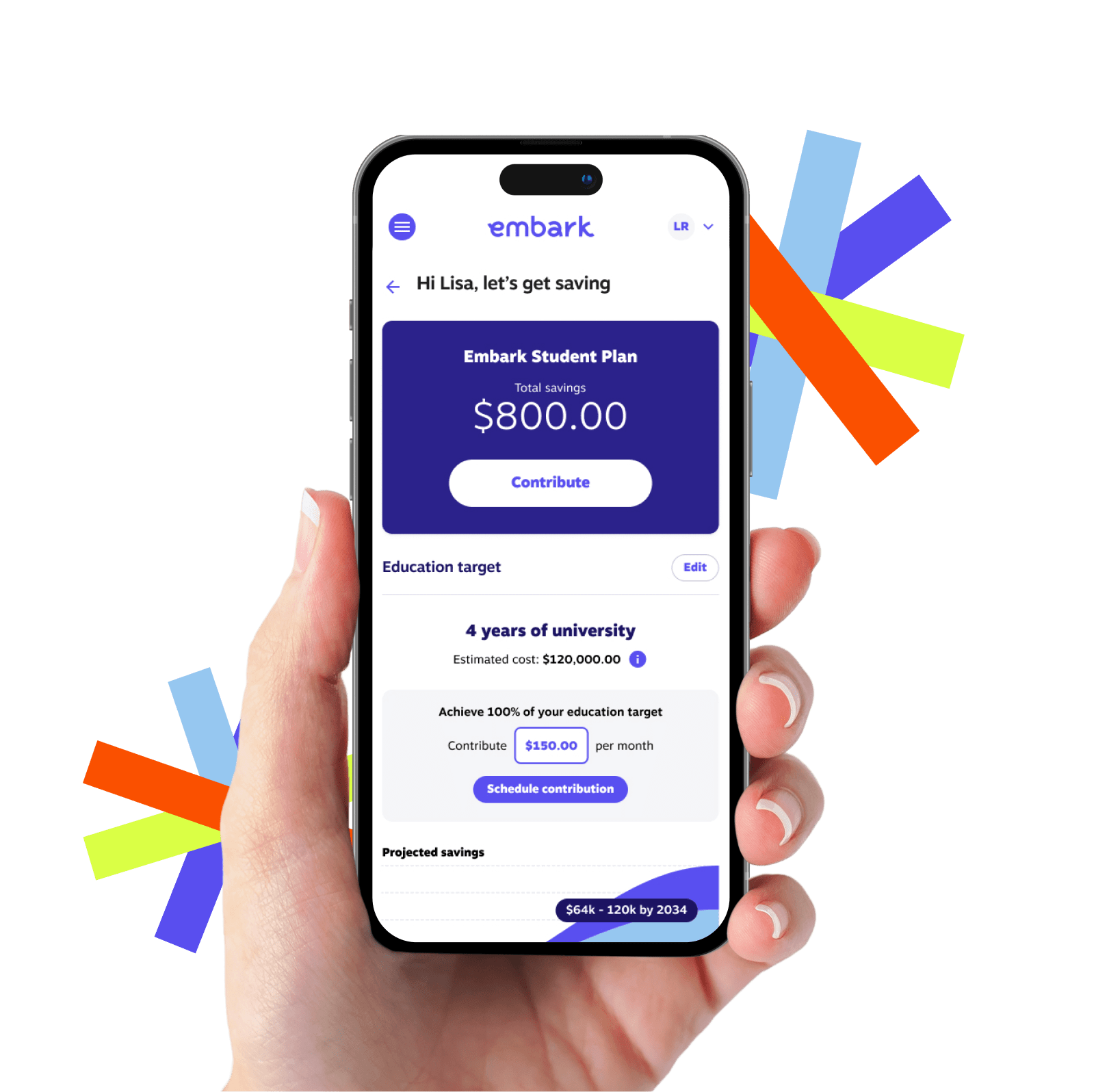

You and your child are moving forward together. Every step gets you closer to everything you hope for and everything they can be. The Embark Student Plan gets you closer to the place where needs and dreams align. It’s one of the most important steps you’ll take to prepare their path to the future.

60,000+

Students who have their post-secondary education costs covered every year with the help of Embark.

1.2 million+

Families and supporters who enjoy the benefits of being part of Embark.

50+ Years

Education savings and planning experience and expertise to help your child be everything they can be.

Guiding Your Education Success

Embark is owned by a not-for-profit organization. This means that all profits that aren’t used to run the business go into the Embark Student Foundation. We use these funds to provide additional financial awards that help students realize their full potential. We’ve awarded almost $57 million to families and students across the country to help with their education savings.

“Easy to access and they take care of

everything for you.”

– Lola O.

All About The Subscriber Vote

The results are in! All Flex First and Family Single Student Plan RESPs will be upgraded to the Embark Student Plan on July 1, 2024.

Learn more about the vote and change today!

Leading the Way to Success

RESP, TFSA or Savings Account – Which is Better?

When it comes to figuring out how to save for your child’s education, you have a few options. Your friends may suggest that you take a look at a RESP, TFSA or a general savings account, but how do you know which is best? Let’s take a look at how each works and find out! Saving […]

6 Minute read

3 Ways to Take the Bite Out of Interest Rates

With inflation soaring in Canada, interest rates are on the rise to help bring prices under control. For savers, this is good news. Rising interest rates mean more money is earned on what you save. For those in debt, this means that more money will have to go toward paying interest and less towards the […]

3 Minute read

When Should You Start Saving For Your Child’s Education?

For many of us, paying for our children’s education is a long-term financial goal. However, with school often so far away, education savings can typically take a back seat to more immediate needs. Take it from an expert though: whether you’re saving a little or a lot, the most important decision you can make when […]

5 Minute read